We know how incredibly easy it is to rack up credit card debt.

More than 40% of American households carry a credit card balance, with an average balance of more than $6,000, according to a study from the financial data website ValuePenguin. The ongoing pandemic has made it even harder for Americans to avoid going into credit card debt, with 20% increasing their overall debt since the start of the pandemic.

But here’s the tricky thing about credit cards: They only benefit you when you’re building credit and receiving perks — but not when you’re paying interest. If you’re paying a lot of interest on your balances, credit card companies are making money off of you.

Your cards are using you, not the other way around.

With average APRs (annual percentage rates) on new credit cards north of 18%, according to WalletHub, paying them off is a smart move. You can do it. And it’ll be worth it.

5 Ways to Eliminate Credit Card Debt

Before you start your journey to becoming debt free, try to stop using your credit cards altogether until you can use them without putting yourself in financial risk. Though the specifics will vary based on your situation, we only recommend using credit cards if:

- You don’t have any debt outside of a mortgage or student loans. (Mortgages and student loan debt are almost impossible to avoid nowadays.)

- You have an emergency fund with three to six months of expenses saved. This is how much money you’d need to survive during that time period, assuming you have no income reaching your bank account.

- You can pay off your credit card debt in full every month — not just minimum payments.

However you do it, make paying off your credit cards — and learning to use them responsibly — a high priority.

First, determine how much credit card debt you have. You can do this using a tool like Credit Sesame , a free credit monitoring service.

Credit Sesame will also show you how to raise your credit score. James Cooper, a motivational speaker, raised his credit score 277 points following suggestions from the site.

Then choose your weapons! We’ll go over five different methods, from debt consolidation loans to repayment strategies to settlement, for paying off your credit card debt.

1. The Debt Avalanche Method

Instead of looking at your debt in its entirety, we recommend approaching it bit by bit. By breaking your debt down into manageable chunks, you’ll experience quicker wins and stay motivated.

Two popular ways to break down debt repayments are the debt avalanche and debt snowball methods.

Using the debt avalanche method, you’ll order your credit card debts from the highest interest rate to the lowest. You’ll make the minimum payment on each of your credit card accounts, and any extra income you have will go toward the highest-interest card.

Eventually, that card will be paid off, and you won’t have to worry about that monthly payment anymore. Then, you’ll attack the debt with the next-highest interest rate, and so on, until all your cards are paid off.

2. The Debt Snowball Method

With the debt snowball method, you’ll order your debts from the lowest balance to highest, regardless of the interest rates on the cards. You’ll make the minimum payment on each of your credit card balances, and any extra income will go to the credit card with the smallest balance.

Starting with the smallest balance allows you to experience wins faster than you would with the avalanche. This method is ideal for people who are motivated by quick wins, but it has a downside: Those who choose it could end up paying more interest over the long term.

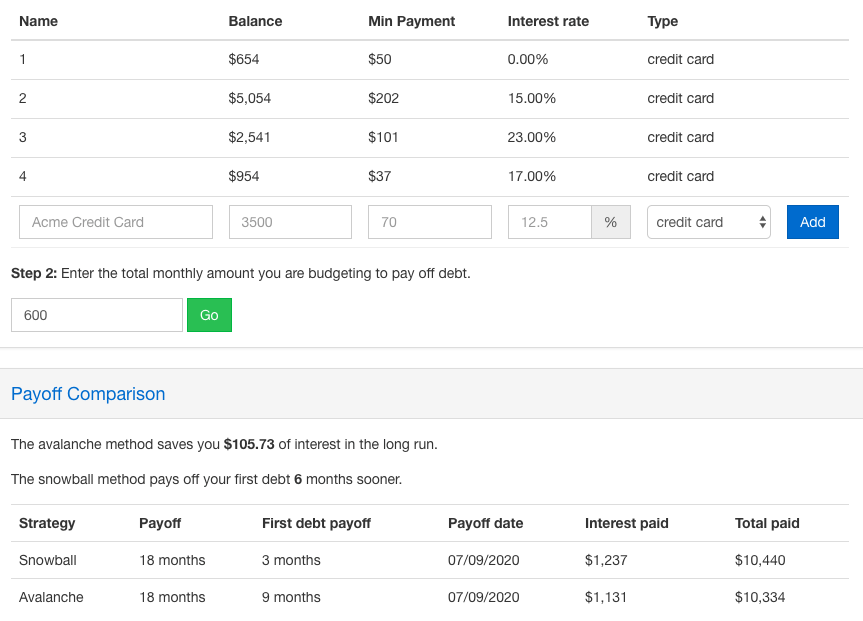

Here’s an example of how each method would work if you’re paying off four credit cards of varying balances and interest rates.

- $654 with 0% interest

- $5,054 with 15% interest

- $2,541 with 23% interest

- $945 with 17% interest

If you followed the avalanche method, you’d pay off card No. 3 first, followed by No. 4, No. 2 and No. 1. If you followed the snowball method, you’d pay off card No. 1 first, followed by No. 4, No. 3 and No. 2.

Let’s say you have $600 per month to put toward debt. Using the snowball and avalanche comparison calculator from Dough Roller , you can see that it would take you 18 months to pay all of your cards off using either method.

The debt avalanche method would save you $105.73 of interest in the end, but you’d pay off your first card six months earlier by going with the snowball.

Choosing the right method comes down to deciding whether you’d rather get quick results or save money on interest. We encourage you to check out Dough Roller’s calculator yourself, so you can calculate what each method would cost you.

3. The Balance Transfer

If you have good to excellent credit (typically a FICO score of 670 or above ) and can feasibly pay off your debt within a year, a balance-transfer credit card is a great option. Balance-transfer cards can save you money on interest charges by letting you transfer the balance of a card with a high interest rate to a card with 0% interest.

Most of these cards offer 0% interest for 12 to 18 months with no annual fee. They generally have a 2% to 5% balance-transfer fee, but you can easily find balance-transfer cards with no fee. A higher credit score will help you qualify for a card with better terms.

4. Take out a Loan

You might look at getting a loan to consolidate and refinance your debts.

If you get a loan with a lower interest rate and pay off your credit cards, that lower rate could potentially save you thousands of dollars in interest.

This is a realistic way to pay off credit card debt if you currently have little or no money to put toward it.

Let’s look at two options for debt consolidation here: A personal loan or a home equity loan.

Personal Loan

Online marketplaces will allow you to prequalify for a personal loan without doing a hard inquiry of your credit, so if you want to shop around, head there first. Shopping for personal loans online does not affect credit scores.

A personal debt consolidation loan is a good idea if you have decent credit and can manage the repayment plan that accompanies the loan. Whereas credit cards offer revolving credit, meaning you can continue to borrow and just make minimum payments, a debt consolidation loan will have a predetermined repayment plan with a set schedule of payments.

A debt consolidation loan is similar to a balance-transfer credit card, as you are consolidating all of your debt into one place. The personal loan route is more attractive, however, because rates are typically lower for debt consolidation loans.

A good resource for finding personal loans here is Fiona, a search engine for financial services, which can help match you with the right personal loan to meet your needs. It searches the top online lenders to match you with a personalized loan offer in less than a minute.

Home Equity Loan

If you own a home with equity, you have three ways to borrow money against the value of your home: a home equity loan, home equity line of credit or a cash-out refinance.

- With a home equity loan, the lender gives you your money all at once, and you repay it at a fixed interest rate over a set period of time.

- With a home equity line of credit, you’re given a limit to borrow. Within that limit, you can take as little or as much as you need whenever you want.

- With a cash-out refinance, you refinance your first mortgage with a mortgage that’s slightly more money than your current one, and pocket the difference.

For homeowners, these options will most likely offer the lowest interest rates. But they’re also the riskiest, because your home is the collateral — something you own that your lender can take if you don’t pay off the loan.

5. Debt Settlement

The world of debt collections and creditors can be confusing, intimidating and sometimes even illegal. There’s a common misconception, for example, that someone can take your house or you can go to jail for not making your credit card payments. But credit card debt is unsecured debt, meaning no one can put you in jail or take your house if you don’t pay it.

If you’re being harassed by creditors or have circumstances that make your debt repayment confusing, don’t give up before finding out your options for assistance.

Debt Management Program

With a debt management program, a credit counseling company will handle your consolidation in hopes of getting you a better interest rate and lower fees. You’ll be assigned a counselor, who will set up a repayment and education plan for you. This program is specifically for unsecured debt, like credit cards and medical bills.

A debt management program pays your creditors for you to ensure you stay current on your debt payments. Your credit score may even improve during the program. But if you miss a monthly payment, you can be dropped, and you’ll lose all the benefits you gained.

Debt management plans usually don’t reduce your debt, but they may reduce your interest rates by as much as half or extend your payment timeline to make paying your debt more manageable.

Credit Card Debt Settlement

If you’re in more than just a temporary season of financial instability, and you can’t see yourself affording the amount of credit card debt you owe, debt settlement is an option, though we regard it as a last resort.

Debt settlement reduces the amount of debt you owe, but it will significantly lower your credit score and negatively impact your credit report.

The process isn’t as simple as debt consolidation. You have to convince every creditor that if they don’t settle with you, they probably won’t get anything at all. So, of course, during that time you won’t be making any payments — while interest and late fees accrue.

You can do this on your own, but most people seek the help of a debt settlement company.

Like a debt management program, a debt settlement firm will negotiate debts on your behalf, and the company will make lump-sum payments to creditors while you make monthly payments to the debt settlement company.

Be careful when seeking help with debt settlement. While some companies are legitimately there to assist you, others take your money and do very little to help your situation.

While you’re paying the debt settlement company, you’ll still be delinquent with any creditors the company hasn’t yet negotiated with, meaning you’ll still get calls from those creditors.

And there’s no guarantee the company will be successful. If it isn’t successful in negotiating, you’ll still be responsible for the full debt amount, plus any extra interest that accrued.

If the company is successful, you’ll have to pay the settlement amount in full. Then in April, you’ll owe taxes on the amount forgiven.

The settlement company will also charge you up to 25% in fees on top of the settlement.

Bankruptcy

Bankruptcy is another last resort. The two major types for individuals are Chapter 7 and Chapter 13.

Chapter 7 bankruptcy allows you to completely discharge all your debts except student loans in four to six months by liquidating your assets. A trustee gathers and sells all of your nonexempt assets to pay off your debt. Those assets can include property that’s not your primary residence, a vehicle with equity, investments or valuable collections.

Those who earn a high income or have significant assets typically choose Chapter 13, which allows you to keep certain assets while still repaying some of the debts. It’s a long, arduous process that doesn’t guarantee to resolve your debt. It can be reversed if your income increases, and it wrecks your credit.

Both bankruptcy options have negative long-term ramifications on your credit. But if you’re out of options, bankruptcy gives you a chance to get your debt under control and get creditors and debt collectors off your back.

How to Pay off Credit Card Debt Fast

If you want to become debt free quickly , here are some ways to pay off credit cards fast:

Up Your Monthly Payments

Make two payments per month instead of one. Most credit card companies use an average daily balance to compute interest charges. Instead of making monthly payments of$400 toward a balance, make two payments of $200, one at the middle of the month and one at the end. You’ll lower the average daily balance so you’ll pay less interest. Some credit card users even advocate for paying off credit card balances every week; a weekly reminder in your calendar is all it takes.

Try to Get a Lower Rate

Ask your credit card companies for lower interest rates. It’s worth trying at least once for each credit card you have. Research competitor cards similar to yours for which you qualify and that offer better rates — then share those with your credit card company to see if they’ll match it.

Knocking four interest percentage points off a $10,000 balance, for example, can save you hundreds of dollars in interest annually. Add those savings to your debt repayment budget!

Get the Debt Reduced

Sometimes you can convince a credit card company to forgive your debt — or at least part of it. After all, these companies want to retain you as a customer, so they may be more open to negotiation than you might think. If you’re in serious financial trouble, explain the situation to the card issuer. Offer to pay a portion of the balance owed as payment in full.

For most of us, though, there’s no quick answer.

How Much Will Paying Off Credit Cards Raise Your Score?

You might be asking yourself, “How much will my credit score go up if I pay off my credit cards?” It turns out that credit card usage has a huge impact on credit scores.

If you spend too much of your overall limit or miss payments, you’ll hurt your score. If you keep your balances low and regularly make your minimum monthly payment on time, your score will increase over time.

Just because you have available credit doesn’t mean you should max out your credit cards. Your credit utilization, which tells the credit bureaus how much of your available credit you’re using, shows whether you are sensible with your borrowing.

Keeping your credit utilization at or under 30% is ideal. That means on a credit card with a $10,000 limit, you wouldn’t want your balance to exceed $3,000.

Credit utilization accounts for a whopping 30% of your score. Other factors affecting your score include payment history (35%), credit history length (15%), credit mix (10%) and new credit (10%).

Credit card issuers make it so easy to get in the habit of overspending. The introductory APR offers, new credit card sign-up bonuses and cash back offers are designed to get us using cards more frequently and thinking less about what items cost.

So if you ever want to be debt-free, you need to change the way you use credit cards.

This was originally published on The Penny Hoarder , which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in